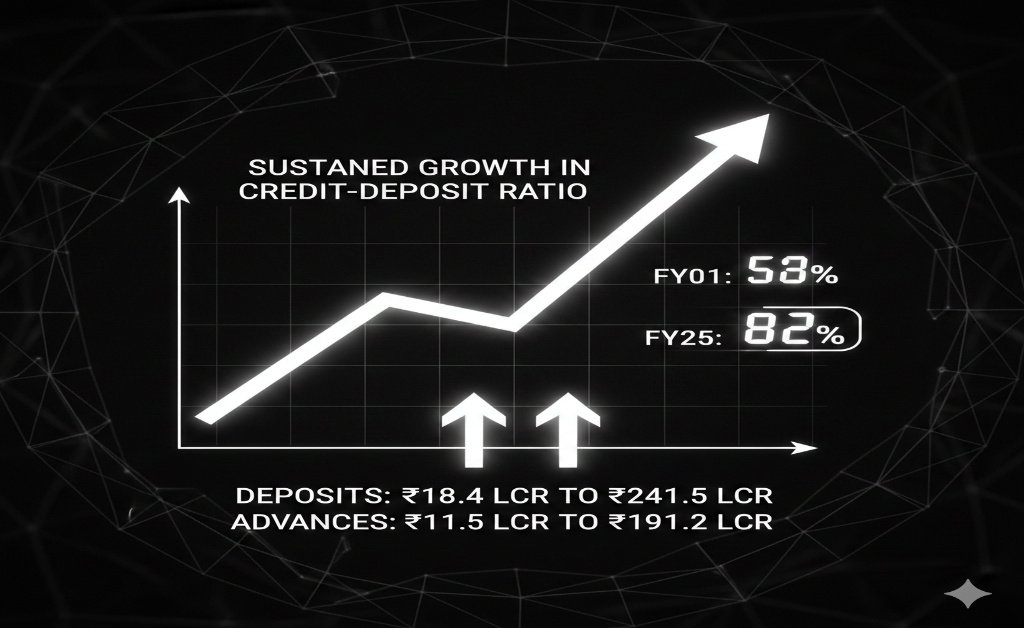

Throughout the 2000s, the Credit-Deposit Ratio of India has experienced an incredible increase, lifting it from just 53% in FY01 to its present day high. The 82% percentage shows that banks are giving out Rs 82 for every Rs 100 they get as deposits. This alteration is mainly due to the “financialisation of the economy,” which is basically a case of people increasingly moving their savings not in the form of physical assets but through the banking system, whence those moneys get to the sectors of economy that are productive. The incremental CD ratio meaning the ratio of new loans to new deposits has been more than 100% in some cases, thereby compelling banks to finance the difference by raising capital through other means like issuing bonds and certificates of deposits.

Strong Post-Pandemic Balance Sheet Revival

The report unveils a really strong Balance Sheet Revival across the whole banking sector. The assets of the banks as the percentage of India’s GDP have shot up drastically to 94%, from 77% in the fiscal year 2021. This rise is due to a big increase in both deposits and advances; in the last twenty years deposits have soared from Rs 18.4 lakh crore to Rs 241.5 lakh crore while advances have gone up from Rs 11.5 lakh crore to Rs 191.2 lakh crore. Public Sector Banks (PSBs) have been the most visible players in this period, gradually recovering market share and signaling “balance sheet repair” after years of dealing with non-performing assets.

Structural Concerns and Deposit Accretion

The high CD ratio has been a cause for concern with regard to liquidity even though there was an increase in deposits. There has been an ongoing scenario of deposits growing slower than credits which has led to the construction of an agencies’ warning around the future lending being constrained. The deposit accretion of the banks is becoming more difficult as investors are transferring their surplus increasingly towards higher-yielding alternative financial instruments like mutual funds. Banks are being urged to innovate their deposit-gathering strategies in order to keep their lending momentum going without breaching the regulatory comfort zones while at the same time tackling the issue of maturity mismatch between short-term deposits and long-term loan portfolios.