The Reserve Bank of India (RBI) has put out a draft proposal that would radically change the way dividends are paid out by Indian banks. The shift of the payment link from total capital to core capital particularly the Common Equity Tier 1 (CET 1) ratio will assist the regulator in developing a more straightforward and risk-sensitive payout structure. The change of policy is very likely to majorly benefit private banks which, on average, hold more core equity than public sector banks.

Core Capital Linkage Effect on Payout Limits

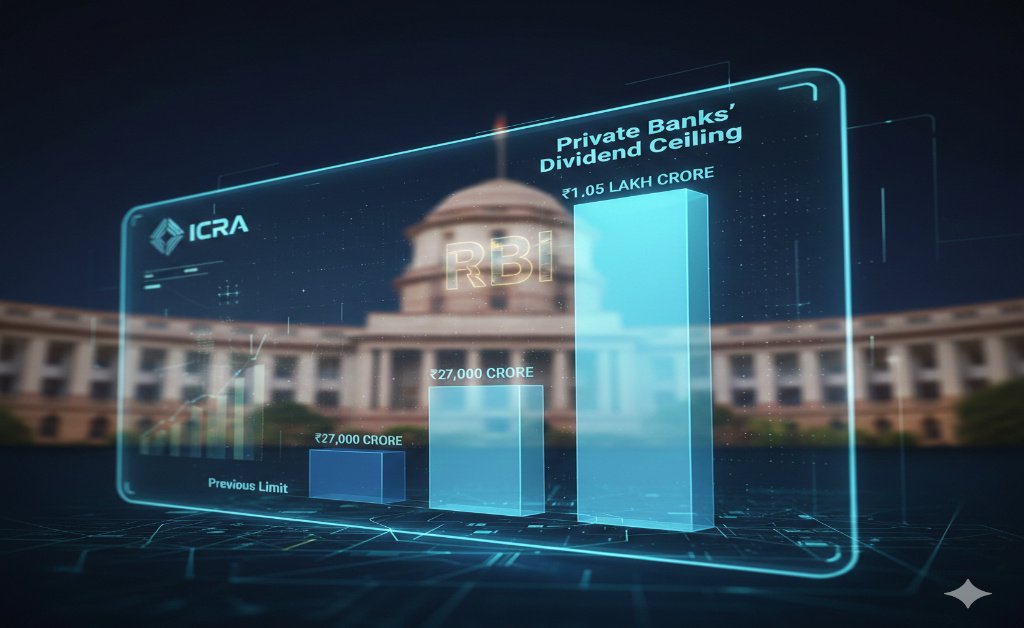

The new RBI proposal suggests the maximum dividend payout ratio for private banks would be significantly improved. ICRA’s analysis predicts that the ceiling for private banks could reach as high as ₹1.05 lakh crore next year, which is a huge surge from the ₹27,000 crore paid in FY25. On the other hand, the ceiling for public sector banks (PSUs) is likely to go up to about ₹70,000 crore as well, but the growth is less vigorous because of their lower CET 1 ratios. The new measure substitutes the previous one based on a bank’s Capital to Risk-Weighted Assets Ratio (CRAR) and net non-performing advances.

Conservative Payout Trends Despite Increased Headroom

Sooner or later, the technical boundaries of dividends will expand, but ICRA predicts a very modest rise in actual dividend payments. The majority of private banks are now paying out less than 20% of their earnings, which is remarkably far from both existing and future ceilings. The banks will be focusing on capital preservation, which is eventually enabling them to grow their credits and to fortify themselves against possible economic downturns. The new regulations will also guarantee that the concept of “adjusted PAT” is followed, meaning that dividends will only be paid from sustainable earnings and not through one-off gains or fair value adjustments.

Divergent Outcomes for Private vs. Public Banks

The amended framework points to an increasing gap between private and government banks. At the moment, the payout ratio of public service unit (PSU) banks is about 20% which is higher than that of private banks at 15%. Nevertheless, the new CET 1-based linkage allows private lenders to have a significantly larger “headroom” for the distribution of funds to shareholders if they decide to do so. There are sixteen major banking institutions, such as seven state-owned and nine private ones, whose limits are going to rise due to the new regulations. At the same time, the largest PSU banks may face a stagnation or a decline of limits under the stricter capital requirements.