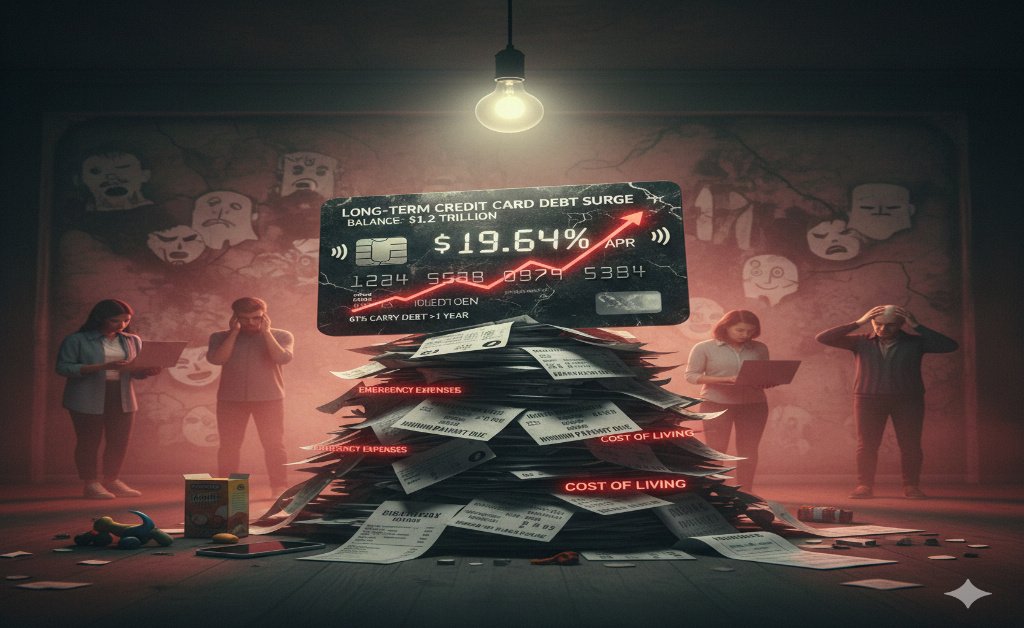

The first month of 2026 has brought about a stark contrast in the credit card scenario worldwide as the U.S. credit card debt continues to skyrocket, while Indian banks are slowly, but surely, adopting a patient approach with regard to their credit card issuance policies. A flood of proposals aimed at relieving the financial burden on consumers has not even been able to change the fact that Bankrate’s 2026 Credit Card Debt Report has classified American users as being trapped under the “debt trap.”

The report on credit card debt by Bankrate discloses a very unhealthy long-term situation, as 61% of the total youngsters in America admit they have been accumulating debt for more than a year, which however is a very big rise when compared to the previous figure of 53% in late 2024. Even though the average interest rates have reached an all-time high and are currently at the level of 19.64% most of the credit card users (47%) do not mind paying interest, they keep on carrying the burden of debt month-to-month. According to the report, everybody involved in the financial juggling act has placed the blame on emergencies (41%) and the increased costs of daily items such as groceries and utilities (33%) as the main reasons why consumers are unable to pay off their debt.

Proposed 10% Interest Rate Cap

The banking sector is one of the few places where the news is predominately good, and the latest sensational story is about the possible imposition of a 10% Interest Rate Cap on credit cards in the U.S. The whole thing has attracted quite a bit of discussion among both policymakers and the financial institutions. The analysts are providing very optimistic estimates that such a cap may lighten the burden of around $100 billion for consumers each year; meanwhile, the respective big banks are ominously predicting “credit curbs” and very limited access to loans for the poorest customers and small businesses. Currently, the highest average APR for such “at risk” categories is as high as 38%, which further widens the already existing “trust gap” in the lending market.

Cautious Credit Issuance in India

The Indian banking sector is showing signs of Cautious Credit Issuance while the U.S. is facing a debt peak of $1.23 trillion. In the recent quarter, the number of new credit card holders fell by 28% compared to the previous year in India as the banks took a defensive position regarding unsecured retail credit and thus their actions. The slowdown in the market doesn’t mean that the average debt per person in India has not gone up; it actually increased by 23% over the last two years, getting to ₹4.8 lakh. The Reserve Bank of India (RBI) is keeping a very close watch and has warned banks to focus on asset quality rather than growth to avoid creating a system-wide “bubble” in consumption-linked borrowing.

Impact on Future Financial Inclusion

The present changes in debt management and regulatory supervision are giving a new direction to the Future Financial Inclusion strategies. In the U.S., the situation is gloomy for the younger generation; for instance, almost 1 in 4 people believe that they will have to deal with debt forever. On the contrary, in India, the major shift towards public sector banks for secured loans is indicative of a move towards the revival of traditional asset-building. The year 2026 is becoming a turning point for both markets, where “Conduct Risk” and “Consumer Protection” are coming forth as the most crucial variables for the stability of the banking sector.